Delta Air Lines Pilot Retirement Benefits: 401(k), MBCBP, and NQDC Explained

Delta pilot retirement benefits rank among the best in commercial aviation. There are four main vehicles: the 401(k) plan, the Market-Based Cash Balance Plan (MBCBP), the Non-Qualified Deferred Compensation plan (NQDC), and the Health Savings Account (HSA). Each works differently, has different contribution limits, and has different rules for when and how you can access the money.

This post explains what each plan is and how it works — no strategy, no advice. Just the facts on what's available to Delta pilots in 2026. For the full compensation picture including base salary and how the pay curve works, see How Much Does an Airline Pilot Make.

At a Glance

| Plan | Funded By | 2026 Limit | Tax Treatment |

|---|---|---|---|

| 401(k) | You + Delta (18% DC) | $72,000 total | Pre-tax, Roth, or after-tax |

| MBCBP | Delta only | Earnings above IRS comp cap | Tax-deferred; taxed at distribution |

| NQDC | You only | 75% flight pay / 100% profit sharing | Pre-tax deferral; taxed at distribution |

| HSA | You + Delta (Health Rewards) | IRS annual limit | Triple tax-advantaged |

Delta Pilot 401(k) Plan

The Delta 401(k) plan is administered by Fidelity. It is the foundation of your retirement package.

Delta's Contribution

Delta makes a non-elective defined contribution (DC) of 18% of your eligible earnings into your 401(k) each year. You receive this regardless of whether you contribute anything yourself.

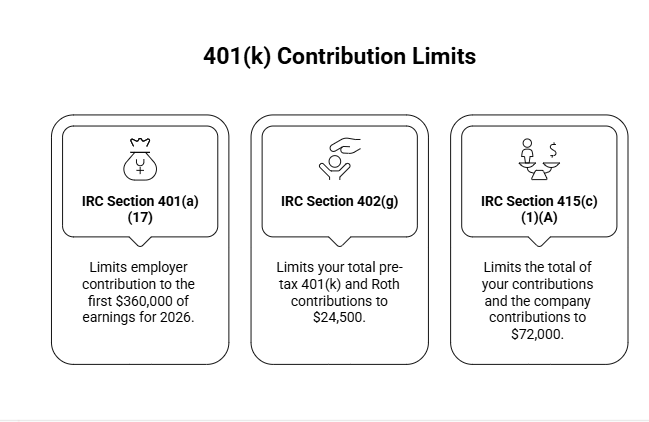

The IRS limits the compensation Delta can base this contribution on to $360,000 in 2026. That means the maximum Delta can contribute to your 401(k) in 2026 is $64,800 (18% × $360,000).

If your earnings exceed $360,000, Delta's 18% on the overage goes somewhere else. This is paid either as a cash payment ("401(k) Excess Plus") or into the MBCBP if you're enrolled.

Your Contribution

Pilot contributions come in two forms: traditional pre-tax 401(k) and/or Roth (after-tax) deferrals, capped at $24,500; and after-tax 401(a) contributions, which fall outside the $24,500 limit but count toward the $72,000 total.

Total Contribution Limit

The IRS caps the combined total of your contributions and Delta's contributions at $72,000 in 2026 (IRC 415(c)). Delta contributes up to $64,800, leaving $7,200 of remaining headroom before hitting the ceiling.

Catch-Up Contributions

Catch-up contributions are available on top of the standard limits and do not count toward the 402(g) or 415(c) limits above.

- Age 50–59 and 64+: $8,000 additional in 2026

- Age 60–63: $11,250 additional in 2026 (SECURE 2.0 "super catch-up")

Under SECURE 2.0, if your FICA wages exceeded $150,000 in 2025, all catch-up contributions in 2026 must be made on a Roth basis.

Investment Options

Your 401(k) offers a lineup of core funds through Fidelity. You also have access to Fidelity BrokerageLink, which opens access to thousands of ETFs, mutual funds, and individual stocks outside the core fund menu.

In-Service Rollover

Starting at age 59½, you can roll your 401(k) balance into an outside IRA while still actively employed. This is called an In-Service Rollover (ISR).

Market-Based Cash Balance Plan (MBCBP)

The MBCBP is a company-funded pension-like plan established on October 1, 2023, as part of a Furlough Avoidance Agreement between Delta and ALPA.

Eligibility

- Pilots hired or rehired on or after June 1, 2023 are automatically enrolled.

- Pilots hired before June 1, 2023 were given a one-time, irrevocable option to opt out, with a deadline of July 31, 2023. Pilots who did not opt out are enrolled.

How It's Funded

Delta funds the MBCBP entirely. You make no contributions. Delta pays all plan administration expenses.

Your account receives two types of credits:

- Base allocations — calculated from your earned pay credits multiplied by an accrual rate. This amount is reduced by whatever Delta has already contributed to your 401(k). In practice, this plan captures the 18% contribution on earnings above the $360,000 IRS compensation cap.

- Interest credits — monthly credits based on the actual investment returns of the plan's assets, net of fees.

Investments

You do not choose investments in the MBCBP. The plan's assets are managed by the Benefits Fund Investment Committee, with a target allocation of 40% global public equities and 60% U.S. intermediate bonds, initially through the BlackRock LifePath Index Retirement Fund.

Vesting

Your MBCBP account is 100% vested at all times.

Accessing Your Money

- In-service withdrawals: Available once per calendar year starting at age 59½, provided your account balance exceeds the total base allocations made to it. The full balance can be withdrawn.

- At retirement or separation: You cannot delay distributions beyond the later of your termination date or the plan's normal retirement age.

Payment Options

At distribution, you can choose:

- Lump sum — full account balance paid at once

- Single Life Annuity — default for unmarried pilots

- 50% Qualified Joint and Survivor Annuity — default for married pilots; 75% option available with spousal consent

Balances of $5,000 or less are automatically paid as a lump sum. If you terminate and make no election, balances between $1,000 and $5,000 are rolled into an IRA; balances under $1,000 are paid directly to you.

Death Benefits

If you die before receiving your benefits, the account is paid to your designated beneficiary. A surviving spouse may choose between a lump sum or a lifetime annuity. A non-spouse beneficiary receives a lump sum.

Non-Qualified Deferred Compensation Plan (NQDC)

The NQDC plan allows eligible pilots to defer a portion of their income beyond IRS-qualified plan limits. It became available in 2026.

Eligibility

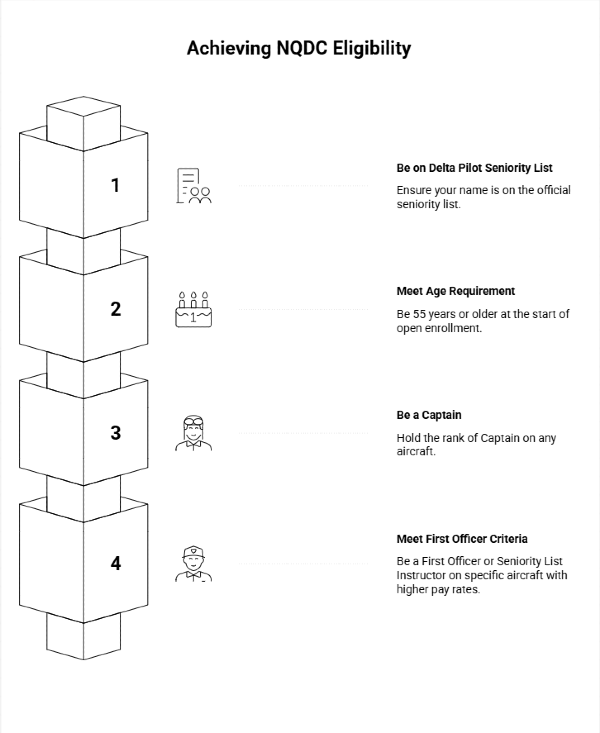

To participate, you must be on the Delta Pilot Seniority List and, at the start of the annual enrollment period, meet at least one of the following:

- Age 55 or older

- Captain on any equipment

- First Officer (or Seniority List Instructor) on the 767-400, A330, A350, or any aircraft with an equal or higher hourly pay rate

What You Can Defer

- Flight pay: Up to 75%

- Profit sharing: Up to 100%

Delta makes no company contributions to this plan.

How Elections Work

You make a new deferral election each plan year. Once the election period closes, your choices are irrevocable for that year. If you begin receiving disability benefits under the Delta D&S Plan or NWA LTD Plan, deferrals automatically pause.

How the Money Is Held

The NQDC is an unfunded plan. Your account is a hypothetical bookkeeping account. The money is not segregated into a separate investment account. You select from available investment options and Delta credits your account to mirror the performance of those funds.

The plan assets are held in a rabbi trust administered by Newport Trust Company. Because it is a rabbi trust, your NQDC balance remains subject to the claims of Delta's general creditors in the event of the company's insolvency. NQDC funds are not protected by ERISA or the Pension Benefit Guaranty Corporation (PBGC).

Vesting

Your NQDC balance is 100% vested at all times.

Distributions

You select your distribution schedule at the time of each annual deferral election. All payouts are made in cash.

- Timing: Payouts begin at the earlier of (a) a specific Distribution Date you elect (always July 1 of a chosen year) or (b) the first day of the second calendar quarter following your separation from service.

- Form of payment: Lump sum or annual installments (at least five installment schedules available). If no valid election is made, the default is a lump sum.

- Changing elections: You can modify your distribution schedule, but only if you submit the change at least 12 months before the originally scheduled payment date, and the new payment date must be at least five years later than the original.

- Hardship withdrawals: Available for an "Unforeseeable Emergency" (severe financial hardship due to illness, casualty loss, or similar). If approved, remaining deferrals for that plan year are canceled.

Death Benefits

You can designate a beneficiary. In the event of your death, your beneficiary contacts Newport Trust to process distribution. If no beneficiary is designated, funds default to your estate.

Health Savings Account (HSA)

The Health Savings Account (HSA) is a tax-advantaged savings vehicle available to pilots enrolled in eligible high-deductible health plans. Administered by Optum Bank, it is designed to help you save and pay for qualified healthcare expenses.

Eligibility & Active Plans

To utilize the HSA as an active pilot, you must be enrolled in an eligible plan, such as the Gold HSA or Silver HSA.

How It's Funded

- Delta's Contribution (Delta Health Rewards): Delta provides Health Rewards (DHR) HSA funding for pilots enrolled in the Gold HSA plan. For 2026, this funding provides up to $850 for employee-only coverage, up to $1,700 for employee plus spouse, up to $1,300 (plus $250 child funding) for employee plus child(ren), and up to $2,150 (plus $250 child funding) for family coverage. The Silver HSA does not receive this company funding.

- Your Contribution: You can contribute your own pre-tax dollars to the account up to the annual limits set by the IRS.

Retirement and COBRA Options

If you retire prior to age 60, you are eligible to enroll in Delta's Retiree and Survivor HSA. For the 2026 plan year, the monthly premiums for this retiree plan are:

- Retiree Only: $1,030.28

- Spouse Only: $1,030.28

- Child(ren) Only: $636.48

Alternatively, you may elect temporary COBRA continuation coverage for your active plans. The 2026 COBRA employee-only premium is $837.85 for the Gold HSA and $695.05 for the Silver HSA.

Protecting Your Funds (FAA Medicals)

Pilots are strongly advised not to use HSA funds to pay for reimbursable FAA medical expenses. To prevent medical providers' systems from automatically associating these bills with your health insurance—which can unnecessarily deplete your HSA balance—you must set up a separate billing account. Use a slight variation of your name for this account (for example, "J. Doe" instead of "John Doe") to ensure the accounts remain completely unlinked.

Frequently Asked Questions

How much does Delta contribute to my 401(k)?

Delta contributes 18% of your eligible earnings each year, up to a maximum of $64,800 in 2026 (18% × the $360,000 IRS compensation cap). You receive this contribution regardless of whether you contribute anything yourself.

Can I contribute to both pre-tax and Roth in my Delta 401(k)?

Yes. You can split your elective deferrals between traditional pre-tax and Roth in any proportion, as long as the combined total stays within the $24,500 limit.

What is the Delta MBCBP and do I have to participate?

The Market-Based Cash Balance Plan is a company-funded, pension-like plan that captures Delta's 18% contribution on earnings above the $360,000 IRS comp cap. Pilots hired before June 1, 2023 had a one-time option to opt out; pilots hired after that date are automatically enrolled with no opt-out.

What's the difference between the Delta 401(k) and the NQDC?

The 401(k) is an IRS-qualified plan with hard contribution limits and ERISA protections. The NQDC lets eligible pilots defer income beyond those limits, but the balance is unfunded and not protected from Delta's general creditors in the event of insolvency.

When can I access my Delta 401(k) while still flying?

You can take in-service withdrawals and roll your balance into an outside IRA starting at age 59½ while still actively employed.

What happens to my NQDC if Delta goes bankrupt?

NQDC balances are held in a rabbi trust but remain subject to the claims of Delta's general creditors. They are not protected by ERISA or the Pension Benefit Guaranty Corporation (PBGC).

This post is for informational purposes only. The plan details and IRS limits described here reflect publicly available information as of 2026 and are subject to change. Nothing in this post constitutes financial, tax, or investment advice. Before making decisions about your retirement accounts, consult a qualified financial advisor who understands the specifics of your situation.